Medicare Supplement Plans 2027

If you’re wondering how to cover the potential out-of-pocket costs not paid by Original Medicare, Medicare Supplement Plans, or Medigap, could be your solution. This guide cuts through the complexity to help you understand the potential costs, benefits, and enrollment process.

Key Takeaways

- Medicare Supplement Plans, or Medigap, provided by private insurers, may cover out-of-pocket costs that might not be included in Original Medicare, such as copayments, deductibles, and coinsurance, but may exclude prescription drug coverage.

- Enrollment in Medigap plans is typically available to those 65 or older during a 6-month period starting after enrolling in Medicare Part B, with issue rights that may prevent denials based on pre-existing conditions; missing this period might lead to higher costs and limited choices.

- Medigap policies will likely be standardized across several plan types with different coverage levels and costs; choosing the right plan will likely require considering individual health needs and financial situation, and costs may be influenced by the insurer’s pricing strategy and policyholder’s demographics.

Compare Plans in One Step!

Enter Zip Code

Understanding Medicare Supplement Plans

Medicare Supplement Plans, or Medigap, could serve a significant purpose in the healthcare insurance landscape. These plans are offered by private insurance companies, and will likely aim to bridge the gaps in Original Medicare coverage.

These gaps may include out-of-pocket costs such as deductibles, copayments, and coinsurance that Original Medicare might not cover. By opting for Medicare supplement insurance, beneficiaries could potentially minimize their financial burden.

When selecting a Medigap plan, remember to consider possible factors such as:

- Coverage options

- Healthcare provider network

- Travel coverage

- Cost

Private insurance companies, regulated by both Federal and state laws, will likely play a pivotal role in providing Medigap plans.

The Role of Private Insurance Companies

Private insurance companies will likely play a fundamental role in providing Medigap plans that may help cover certain out-of-pocket expenses, such as copays, coinsurance, and deductibles, that may not be included in Medicare coverage.

These may be subject to stringent regulations by both Federal and state laws to potentially ensure consumer protection.

When looking to buy a Medigap policy, you should contact any insurance company licensed to sell Medigap in your state.

Choosing the Right Plan

Selecting the most suitable Medigap plan will likely be an integral step toward obtaining comprehensive healthcare coverage. This may involve considering your current health requirements, anticipating potential future needs, and assessing the coverage options of various plans.

Keep in mind that certain Medicare Supplement Plans might offer coverage for emergency medical expenses incurred while traveling outside the United States.

Members could avoid mistakes such as missing the initial enrollment period, signing up for the wrong coverage, and choosing a plan based on someone else’s recommendation.

Best Medicare Supplement Plans 2027

When evaluating the best Medicare Supplement (Medigap) plans for 2027, most beneficiaries narrow their focus to a small group of standardized options that deliver the strongest balance of coverage, premium stability, and long-term value.

Because all Medigap plans are federally standardized, the benefits for each plan letter are identical across carriers—meaning the decision often comes down to plan design, pricing, and rate history rather than differences in coverage.

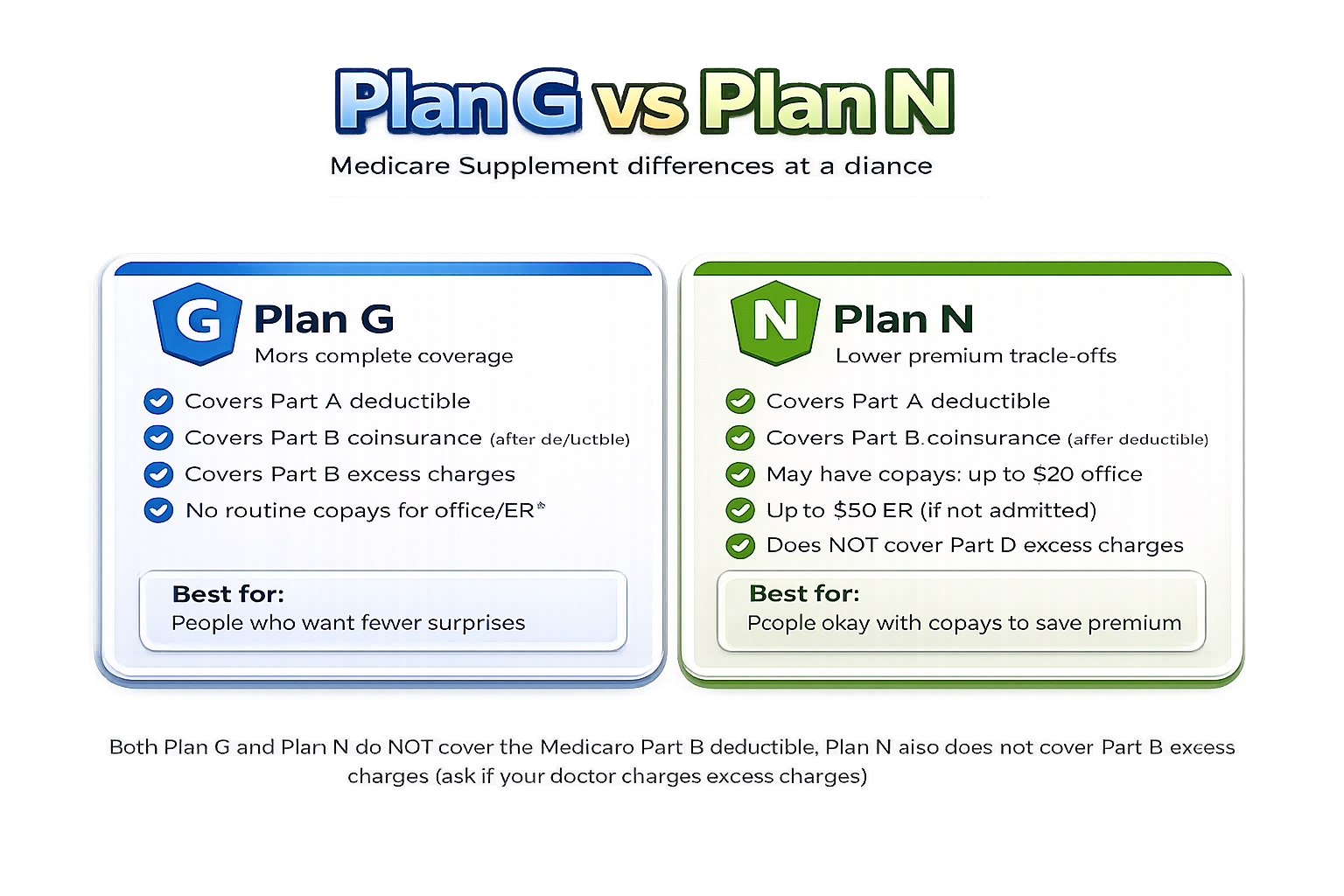

Medicare Supplement Plan G (Top Comprehensive Option)

Medicare Plan G continues to be the most popular and comprehensive option available to new enrollees in 2027. It covers nearly all out-of-pocket costs associated with Original Medicare, including Part A coinsurance, hospital costs, skilled nursing facility coinsurance, hospice care, and Part B excess charges.

The only cost not covered under Plan G is the Medicare Part B deductible. Once that deductible is met for the year, Plan G effectively provides near “full coverage,” eliminating most additional medical expenses.

For beneficiaries who want predictable healthcare costs and minimal out-of-pocket exposure, Plan G remains the benchmark. It also tends to have a more stable rate increase over time compared to older plans, making it a strong long-term choice.

Medicare Supplement Plan N (Cost-Efficient Alternative)

Plan N is often considered the best value option for beneficiaries who want solid coverage at a lower monthly premium. While it includes many of the same core benefits as Plan G, there are a few cost-sharing components to be aware of:

- Copayments of up to $20 for doctor visits

- Up to $50 for emergency room visits (if not admitted)

- Does not cover Part B excess charges

Because of these trade-offs, Plan N works best for individuals who are relatively healthy, do not see providers frequently, and want to reduce their monthly premium costs. In many cases, the premium savings outweigh the occasional copay expenses.

One key consideration is provider billing practices—if you live in a state where excess charges are common, Plan G may offer better financial protection.

High-Deductible Plan G (Lowest Premium Strategy)

High-deductible Plan G has gained traction as a strategic option for cost-conscious enrollees in 2027. It offers the exact same coverage as standard Plan G—but only after you meet a significantly higher annual deductible.

This deductible (set annually by Medicare) must be paid out-of-pocket before the plan begins covering costs. In exchange, premiums are substantially lower—often the lowest among comprehensive Medigap options.

This plan is best suited for:

- Individuals who want catastrophic coverage protection

- Those comfortable with higher upfront risk

- Beneficiaries who rarely use medical services

From a financial standpoint, High-Deductible Plan G can be a powerful tool for managing long-term healthcare costs, especially for those prioritizing premium savings over first-dollar coverage.

Medicare Supplement Plan F (Closed to New Enrollees)

Plan F is no longer available to newly eligible Medicare beneficiaries (those who became eligible after January 1, 2020), but it remains an important part of the Medigap landscape in 2027.

For those who are still eligible and enrolled, Plan F offers the most comprehensive coverage available. It covers everything that Plan G does—plus the Medicare Part B deductible. This results in true “first-dollar coverage,” meaning virtually no out-of-pocket costs for covered services.

However, there are two major considerations:

- Plan F premiums are typically much higher than Plan G premiums

- Because the plan is closed to new enrollees, its risk pool may age over time, potentially leading to higher rate increases

For many beneficiaries, Plan G has effectively replaced Plan F as the preferred comprehensive option due to its lower premiums and more favorable long-term outlook.

Compare Plans in One Step!

Enter Zip Code

Eligibility and Enrollment

The first step to becoming a member of a Medigap plan is to enroll in Medicare Part A and Part B. You can enroll in Medicare Supplement Plans during the 6-month Medigap Open Enrollment period, which begins the first month you have Medicare Part B and are 65 years old or older.

This period gives you guaranteed issue rights, meaning insurance companies can’t refuse you coverage or charge you more because of pre-existing conditions. However, it’s worth noting that private insurance companies may decline seniors for Medigap insurance policies after their initial enrollment in Medicare.

To enroll, call one of our licensed agents at 1-833-641-4938 (TTY 711), Mon-Fri 8 am-9 pm EST. They can provide comprehensive information, personalized guidance, and ongoing assistance to navigate the enrollment process for private insurance companies, making it easier for beneficiaries to make informed decisions about their healthcare.

When to Enroll: Open Enrollment Period

The Open Enrollment Period, a significant time frame for Medigap plan enrolment, spans over a 6-month duration, commencing from the month one acquires Medicare Part B and attains the age of 65 or older.

Missing the Open Enrollment period may lead to increased premiums and restricted coverage options, as there might not be any federal assurance that an insurance company could offer you a Medigap policy if you are beyond the Open Enrollment period.

Qualifying for Medigap

Qualifying for a Medigap policy involves meeting several eligibility criteria, including:

- Age: Individuals must be at least 65 years old or older.

- Disability: Some states offer Medigap policies to individuals under 65 who have a disability.

- Residency: The primary address must be in the state where the individual spends most of the year.

These are just some of the potential factors that could affect whether an individual is eligible for a Medigap policy.

It’s also important to note that an individual’s health status or pre-existing conditions may also impact their eligibility for Medigap.

Switching Plans or Providers

Life circumstances and needs can change, and with them, your Medigap plan might need to change too. It is possible to switch Medigap providers if an insurer is willing to offer you a new policy.

However, a waiting period of up to 6 months may apply before new benefits or pre-existing conditions are covered when switching to Medigap plans.

To discontinue your Medigap policy, you should contact your insurance company and request cancellation.

Standardized Medigap Plans Explained

Medicare Supplement Plans will likely be standardized across distinct categories, denoted by letters A-D, F, G, and K-N. One of the potential distinguishing factors between Medigap plans with the same letter, which may be offered by different insurance companies, will likely be the price.

Potential Benefits Offered by Each Plan

Each Medigap plan may offer potential benefits that could come with varying levels of coverage. For example, Medigap Plan A might provide some of the fundamental benefits without any additional extras, while Medigap Plan B may offer coverage similar to Plan A, with the possible addition of covering the Medicare Part A deductible and possibly increased hospitalization coverage.

Medigap Plan C will likely encompass the benefits provided by Medicare Supplement Plans A and B, and may also include coverage for skilled nursing facility coinsurance and foreign travel emergency coverage.

Possible Premiums, Deductibles, and Out-of-Pocket Costs

Comprehending the potential costs linked with Medigap plans could be vital. Premiums for these plans will likely be determined via three methods: community-rated, issue-age-rated, and attained-age-rated.

Deductibles represent the amount that individuals must pay before the plan begins covering their Medicare out-of-pocket expenses.

Medigap policies may serve to cover some of the individual’s portion of out-of-pocket costs, which may include deductibles, copayments, and coinsurance, which may not be included in the coverage provided by Original Medicare.

How to Determine the Best Plan for You

Selecting the right Medigap plan will likely be a personal decision, depending on one’s healthcare needs and financial conditions. This may involve assessing your current health needs, future requirements, and evaluating the possible benefits, costs, and coverage of various plans.

To compare the potential benefits of Medigap plans, you can use this website by entering your zip code into any of the zip code boxes on this page. By doing so, you can also:

- Compare different Medicare Advantage and Prescription Drug Plans

- Focus on drug coverage and costs to find the perfect fit for your healthcare needs

- Input your information and sort through a variety of plans

- Weigh the pros and cons of each based on your situation

Potential Financial Considerations for Medigap Policyholders

Owning a Medigap policy may also entail certain financial considerations. Familiarizing oneself with cost estimation, expense management, and navigating price changes could be vital.

It may be important to note that Medigap policy prices may change annually.

Estimating Your Costs

Estimating the costs of a Medigap policy will likely involve comparing the prices of the plans that could be offered by insurance companies. Possible factors such as your health conditions, the methodology insurers may employ to determine premiums, and your geographical location, could also influence the cost.

However, the premiums for a Medicare Supplement plan may vary depending on various factors such as the plan type, the company providing the plan, and your location.

Managing Expenses

Managing your Medigap-related expenses effectively could be imperative. Some strategies for managing the potential expenses associated with Medigap coverage may include:

- Purchasing a Medigap policy that could address gaps in Original Medicare coverage

- Understanding the various pricing methods for Medigap policy premiums

- Using Medigap policies to potentially mitigate out-of-pocket costs linked to Original Medicare.

The selection of a Medigap plan could influence overall healthcare costs by potentially providing coverage for the approximate 20 percent that will likely be the individual’s responsibility to pay, as well as other out-of-pocket expenses.

Navigating Potential Price Changes

Some of the Medigap plan prices may undergo an annual change. Policyholders will likely be notified about price changes through telephone and traditional mail.

The possible changes in pricing for Medigap plans may be influenced by a variety of factors, including:

- The insurance company

- The specific plan type

- The policyholder’s age

- Location

- Gender

- Health status

- Tobacco usage

Possible Services Covered by Medigap

Certain Medigap plans may provide supplementary benefits such as vision, dental, and hearing services.

Excess Charges Coverage

Excess charges refer to the additional amount that a doctor may charge above the Medicare-approved amount. These charges may also be known as Part B excess charges and might be covered by certain Medigap plans.

Medigap Plan F and Medigap Plan G might provide coverage for excess charges, which may include Medicare Part B excess charges.

Other Possible Services

Although healthcare services may be crucial, members may want to note that certain Medigap plans may also provide coverage for:

- routine vision care

- routine dental care

- routine hearing care

Comparing Providers and Plans

Selecting the appropriate Medigap plan and insurance provider could be a key step toward securing comprehensive healthcare coverage. Various potential factors, which may include the insurance company’s reputation, plan availability and possible restrictions, and the quality of customer service and support, should be considered.

Reputation and Reliability of Insurance Companies

Choosing a reputable and reliable insurance company for your Medigap policy could be crucial for ensuring a smooth and satisfactory experience. Companies with a favorable reputation might offer:

- High-quality policies that could cater to the requirements of beneficiaries

- Superior customer service

- Dependable claims processing

- A history of providing extensive coverage

Plan Availability and Restrictions

The availability and potential restrictions of certain Medigap plans may vary based on several factors.

While it may be possible to purchase Medigap policies from any insurance company that has been licensed to sell in your state, certain health conditions may also impact the availability and possible limitations of Medigap plans.

Customer Service and Support

Good customer service will likely be a cornerstone of a satisfactory experience with any insurance provider.

Companies may provide:

- Accessible and knowledgeable customer service representatives

- Predictable pricing

- Sufficient coverage

- Offer a variety of policy options

- Emphasize customer experience and loyalty

Summary

This article has provided a comprehensive guide to understanding the possible Medicare Supplement Plans, their potential benefits, costs, and how they could be tailored to individual needs.

From understanding the role of private insurance companies in providing these plans to the eligibility criteria, enrollment process, and various financial considerations, this article has covered some of the potential aspects of Medigap policies.

As healthcare needs and financial circumstances may vary for everyone, it’ll likely be crucial to choose a Medigap plan that can cater to your specific needs.

Remember, good healthcare coverage might not just be about managing current health conditions, but also about anticipating future needs and possibly ensuring comprehensive coverage.

Compare Plans in One Step!

Enter Zip Code

Frequently Asked Questions

→ What is one of the more popular supplement plans for Medicare?

One of the popular supplement plans for Medicare will likely be Medigap Plan F, although Plan G may become more popular for new Medicare beneficiaries due to recent legislation.

→ What is the average price of a Medicare supplemental plan?

The average cost of a Medicare supplemental plan will likely vary depending on potential factors such as age, location, and the specific plan chosen.

→ Do you need supplemental insurance with Medicare?

Yes, you may need supplemental insurance with Medicare to cover potential gaps and expenses that might not be covered by Parts A and B, such as deductibles.

→ What are Medicare Supplement Plans?

Medicare Supplement Plans, also known as Medigap, may help cover certain out-of-pocket costs that may not be covered by Original Medicare, such as deductibles, copayments, and coinsurance, and will likely be offered by private insurance companies.

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 15 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.