Navigating the intricacies of healthcare can be overwhelming, particularly as you approach retirement. One way to alleviate these challenges is by considering supplement insurance, often referred to as Medigap, for peace of mind.

When Original Medicare doesn’t cover all your healthcare expenses, a Medigap policy steps in to fill the financial gaps. Medigap, or supplement insurance, acts as extra insurance you can buy, designed to cover expenses that can catch you off guard, such as deductibles, copayments, and coinsurance.

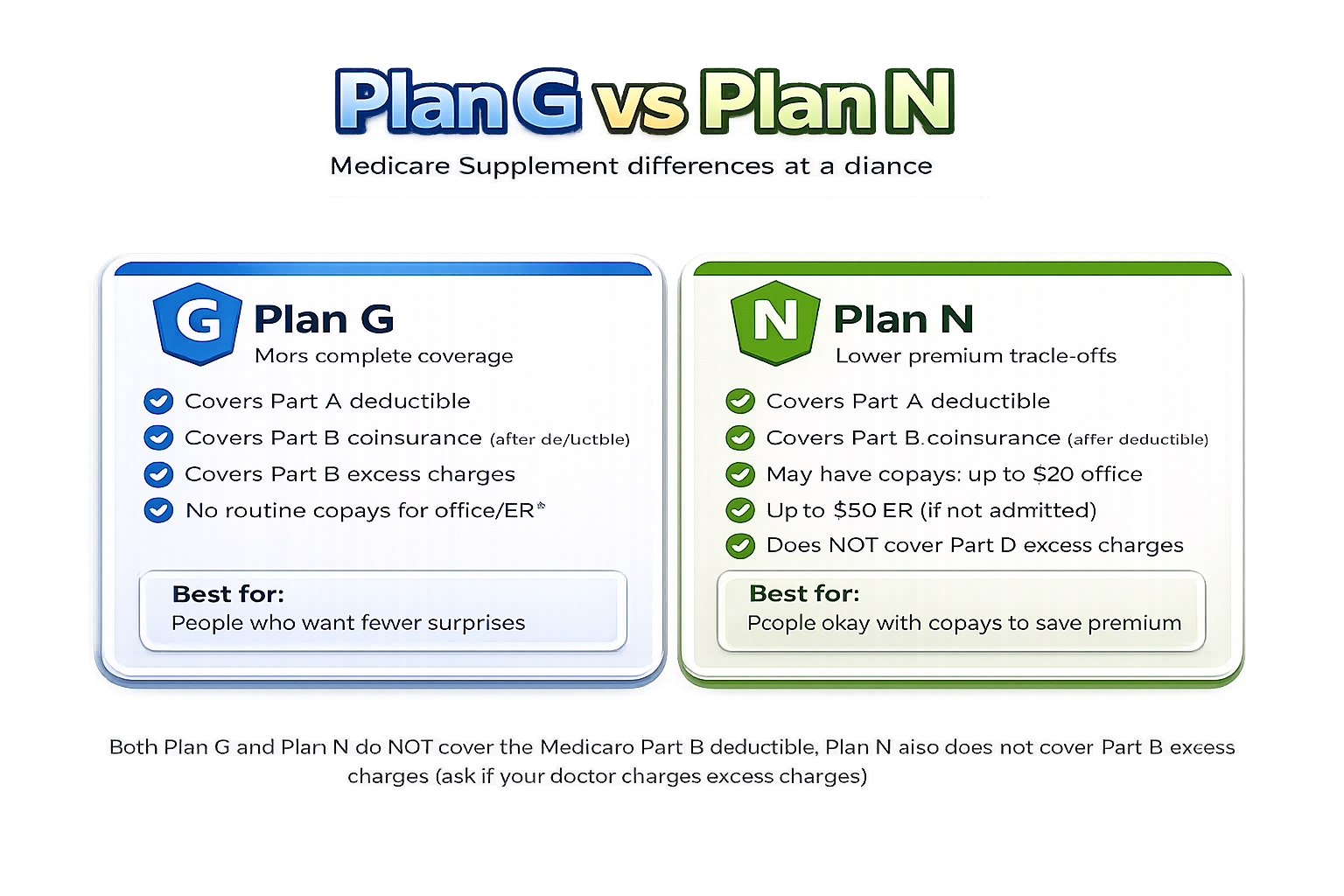

Supplement insurance plans, standardized by the government, ensure that whether you opt for Plan A or Plan G, the core benefits remain consistent across different private companies offering these plans.

While the benefits do not vary, the premiums can, depending on your provider, such as Humana, which competes in this space. This consistency simplifies decision-making, allowing you to focus on comparing costs and understanding how each plan fits your healthcare needs.

Using a supplement plan means more predictability with out-of-pocket expenses, particularly in areas like hospitals or other healthcare services not fully covered by Original Medicare.

This predictability allows for better healthcare planning and helps maintain financial stability. For instance, if Medicare covers 80% of a medical bill, your Medigap policy could cover the remaining 20%, minimizing unexpected expenses.

Medigap plans don’t just provide financial relief, they offer the comfort of knowing you have access to a wide array of healthcare providers nationwide. Unlike some plans that may have restrictive networks, a Medigap member can visit any hospital or doctor that accepts Medicare.

This is especially beneficial if you travel frequently or live in different states throughout the year, ensuring continuous and consistent care.

For those considering supplement insurance for 2027, it is crucial to weigh the benefits of these standardized plans against your personal health needs and financial situation.

Supplement plans offer comprehensive coverage, reducing worry and allowing you to focus on maintaining your health rather than stressing over potential medical costs.

Consider entering your ZIP code below to explore options in your area or contacting an independent Medicare advisor for insightful guidance tailored to your unique situation.

Exploring Medicare Supplement Plans for 2027 can be an important step in meeting your healthcare needs. Take your time to understand the diverse options available and how each one may align with your circumstances. For a more detailed comparison, enter your ZIP code on our site.

This can help you browse plans specific to your area. Additionally, our resources are here to provide guidance and insights into Medicare coverage as you make informed decisions.

Stay confident and knowledgeable as you navigate your Medicare Supplement choices.