Medicare Advantage Plans South Carolina 2026

Curious about the potential Medicare Advantage plans in South Carolina

Key Takeaways

- South Carolina will likely offer several Medicare Advantage plans, likely providing access to comprehensive coverage and sometimes additional benefits that could go beyond Original Medicare.

- Three main types of Medicare Advantage plans available are HMO, PPO, and SNPs, each catering to different healthcare needs and preferences.

- Enrollment options include specific periods throughout the year, with an emphasis on the Annual Enrollment Period from October 15 to December 7, allowing beneficiaries to review and change their plans.

Compare Plans in One Step!

Enter Zip Code

Understanding South Carolina Medicare Advantage Plans 2026

South Carolina residents will likely have numerous Medicare coverage options, with approximately 97 Medicare Advantage plans available, possibly guaranteeing that every Medicare beneficiary in South Carolina could have access to at least one plan. Certain plans, likely offered by reputable insurance companies like Aetna, BlueCross BlueShield, and Cigna, might come with additional benefits that Original Medicare does not provide, such as prescription drug coverage, dental, vision, and hearing coverage.

These plans could potentially offer comprehensive coverage and sometimes additional benefits, possibly making them an attractive choice for enhancing Medicare coverage.

Types of South Carolina Medicare Advantage Plans Available

Medicare Advantage plans in South Carolina are categorized into three types: Health Maintenance Organization (HMO) plans, Preferred Provider Organization (PPO) plans, and Special Needs Plans (SNPs). Each plan type offers unique features and coverage options, likely catering to the diverse needs of beneficiaries.

Knowing the differences between these plans could help in choosing the one that best fits your healthcare needs.

HMO Plans

HMO plans require members to choose a primary care physician and obtain referrals for specialist care, ensuring coordinated and cost-effective healthcare. Some HMO plans might offer lower premiums compared to Original Medicare. Members must use a network of doctors and hospitals, except in emergencies, which could help control costs.

HMO plan members should confirm that their preferred doctors are within the network due to limited provider options. The need for referrals and network restrictions may be balanced by the potential reduction of out-of-pocket costs and improved care management, likely making HMO plans a popular choice among beneficiaries seeking coordinated care.

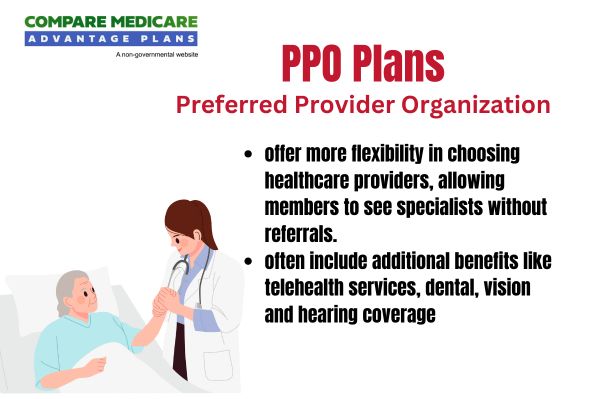

PPO Plans

PPO plans offer more flexibility by allowing members to see any healthcare provider without a referral, though costs might be lower when using in-network providers. PPO plans provide this flexibility, allowing members to choose healthcare providers both in and outside of their network, as long as those providers accept Medicare terms. This could be particularly advantageous for members seeking specialized care without the need for referrals.

Using in-network providers could potentially result in lower out-of-pocket costs. Some PPO plans may also provide additional benefits such as dental, vision, and hearing coverage. The ability to see out-of-network providers could give beneficiaries more freedom, although it may come at a higher cost.

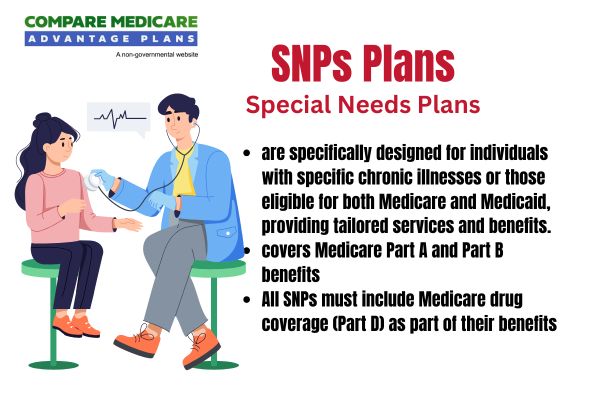

Special Needs Plans (SNPs)

Special Needs Plans (SNPs) are tailored for individuals with specific health needs, such as chronic illnesses or those who reside in institutions. There will likely be several SNPs types available, including Dual-Eligible Special Needs Plans (D-SNPs) for those who qualify for both Medicare and Medicaid, Chronic Condition Special Needs Plans (C-SNPs) for those with specific chronic conditions, and Institutional Special Needs Plans (I-SNPs) for individuals residing in skilled nursing facilities.

These plans could provide specialized care and benefits, possibly ensuring that members receive the appropriate support for their specific health conditions.

Overview of South Carolina Medicare Advantage Plans 2026

Medicare Advantage plans in South Carolina are private managed care options that offer standard Medicare benefits and sometimes additional benefits. There were about 97 Medicare Advantage plans available in recent years, a slight increase from the previous years, likely reflecting the growing options for beneficiaries. Some plans may include additional benefits such as prescription drug coverage, dental, vision, and hearing coverage.

South Carolina residents with Medicare will likely have access to a Medicare Advantage plan. Insurance providers like Aetna and BlueCross BlueShield of South Carolina may also offer various Medicare Advantage plans that could cater to different health needs, possibly ensuring that every beneficiary could find a plan that matches their requirements.

Covered Services and Potential Benefits

Some Medicare Advantage plans may include prescription drug coverage, and dental, vision, and hearing services. These additional benefits could potentially provide comprehensive care and support for beneficiaries, possibly ensuring they have access to

These extensive benefits could potentially make Medicare Advantage plans a robust choice for comprehensive healthcare coverage.

Possible Benefits of South Carolina Medicare Advantage Plans 2026

Some Medicare Advantage plans may offer additional benefits that could go beyond standard Medicare services, such as dental, vision, and hearing coverage. Certain Medicare Advantage plans may also provide integrated prescription drug coverage, possibly streamlining healthcare management for participants. This potential integration might not only simplify the process but could potentially ensure that beneficiaries receive comprehensive care without the need for multiple plans.

Enrollment Process for South Carolina Medicare Advantage Plans 2026

The enrollment process for Medicare Advantage plans allows individuals to join, switch, or drop plans during specific periods throughout the year. Before enrolling, individuals must confirm their eligibility for South Carolina Medicare Advantage Plans to ensure they meet the necessary criteria.

When to Enroll

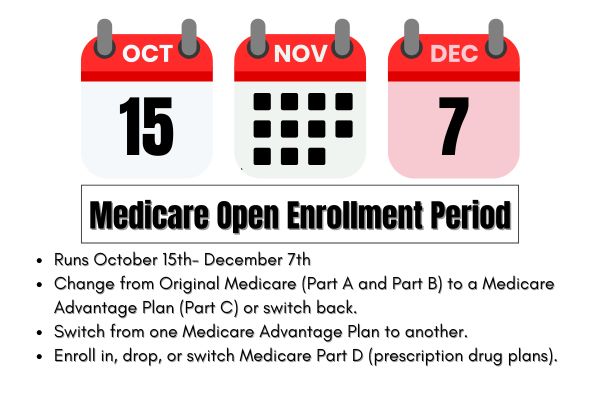

The annual open enrollment period takes place from October 15 to December 7 each year, during which beneficiaries can make changes to their Medicare Advantage plans. This period is crucial for those looking to switch plans, enroll in a new plan, or drop their current plan. For individuals first becoming eligible for Medicare, the initial enrollment period typically occurs around their 65th birthday, providing a seven-month window to sign up for a plan.

If a beneficiary’s current plan is discontinued for the following year, they must enroll in a new plan by December 31 to maintain continuous coverage starting January the following year. There is a Special Enrollment Period for individuals to enroll in a new plan, which runs from December 8 to February 28.

This flexibility likely ensures that beneficiaries can maintain their healthcare coverage without interruption.

Different Enrollment Periods

There are several key enrollment periods for Medicare Advantage plans, including the Initial Enrollment Period for newly eligible individuals, the Annual Enrollment Period, and the Special Enrollment Period for those with qualifying life events. The Initial Enrollment Period allows new Medicare beneficiaries to sign up for a plan starting three months before their Medicare coverage begins and ending three months after. This period provides a generous window for new enrollees to choose the best plan for their needs.

The Annual Enrollment Period runs from October 15 to December 7, during which individuals can join, switch, or drop their Medicare Advantage Plans.

Additionally, the Medicare Advantage Open Enrollment Period occurs from January 1 to March 31, allowing current enrollees to switch plans or revert to Original Medicare.

Special Enrollment Periods are available under certain circumstances, such as relocation or loss of coverage, allowing beneficiaries to enroll outside the usual periods.

OEP, AEP, and Special Enrollment

The Annual Enrollment Period (AEP) runs from October 15 to December 7 each year, allowing beneficiaries to switch plans or enroll in new Medicare Advantage plans. This is the most common time for making changes, as it provides a window for beneficiaries to review their current coverage and explore new options. If changes are made during this period, the new coverage will begin on January 1 of the following year.

The Open Enrollment Period (OEP) runs from January 1 to March 31, allowing individuals already enrolled in a Medicare Advantage Plan to switch plans or revert to Original Medicare.

Special Enrollment Periods (SEPs) are also available for beneficiaries who experience certain life changes, such as moving or losing health coverage, enabling them to enroll or change plans outside standard periods. This flexibility could ensure that beneficiaries can adapt their healthcare coverage to their changing circumstances.

Potential Costs Associated with South Carolina Medicare Advantage Plans 2026

Medicare Advantage plans may feature competitive pricing compared to Original Medicare, potentially leading to lower overall healthcare costs. Knowing the various costs associated with these plans could help in budgeting and making informed healthcare decisions.

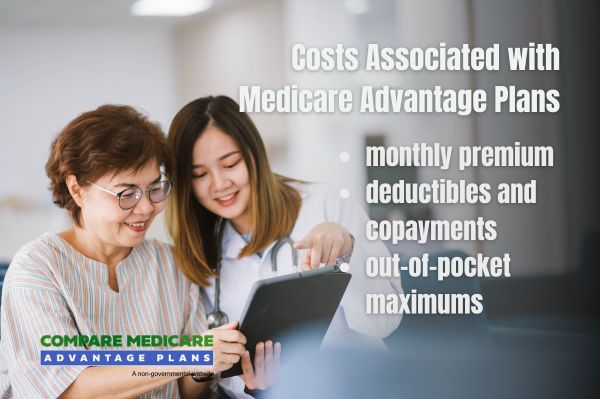

Premiums and Co-Pays

The cost of the monthly premiums and copays of Medicare Advantage plans may vary depending on the specific plan and coverage options. Medicare Advantage plans will likely offer various plans with different premium structures, possibly allowing members to choose based on their financial situation.

Out-of-Pocket Maximums

Some Medicare Advantage plans may provide an out-of-pocket maximum, possibly offering financial protection for members. This potential cap on out-of-pocket costs may be applicable to certain services covered under the Medicare Advantage plan, which might include a variety of medical services.

This potential out-of-pocket maximum could potentially protect beneficiaries from excessive healthcare costs during the year, possibly providing peace of mind.

How to Qualify for South Carolina Medicare Advantage Plans 2026

To qualify for a Medicare Advantage plan, individuals must meet the following criteria:

- Be eligible for Medicare, which typically requires them to be 65 years or older or to have certain disabilities.

- Reside in the service area of the plan they wish to join.

- Be enrolled in both Medicare Part A and Part B.

Some plans may have specific eligibility requirements based on health conditions or prior enrollment in other Medicare plans, and enrollees might need to provide documentation to verify eligibility.

Contracted Network and Access to Care

Medicare Advantage plans will likely include a network of healthcare providers, which may allow members to receive care at lower costs when using in-network services. Access to specialists in the network might require a referral, especially for PPO plans, possibly providing flexibility for members seeking specialized care. Members may also have the option to see out-of-network providers, although this might incur higher costs.

To manage one’s healthcare effectively, members should choose a primary care provider within their network. This broad access to care could make these plans a reliable choice for beneficiaries.

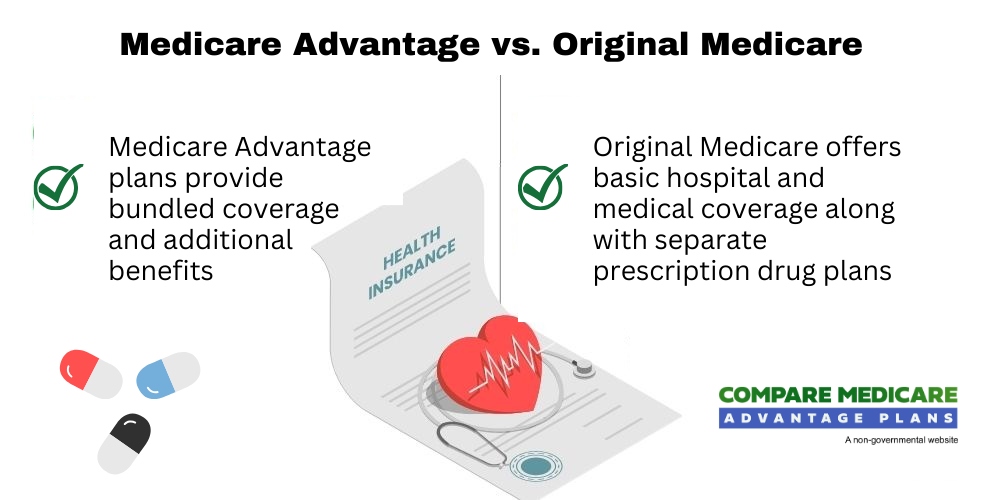

Comparing Medicare Advantage Plans to Original Medicare

Comparing Medicare Advantage plans to Original Medicare could be crucial for understanding the potential differences in coverage, cost, and provider access.

Coverage Differences

While Original Medicare covers most necessary services, some Medicare Advantage plans may include additional benefits not found in Original Medicare, such as dental, vision, and hearing coverage. Unlike Original Medicare’s fee-for-service model, Medicare Advantage plans might require prior authorization for certain services and may include cost management strategies like HMOs or PPOs.

Beneficiaries must weigh these differences when choosing between the two options.

Cost Comparisons

Some Medicare Advantage plans may set an annual limit on out-of-pocket costs for covered services, unlike Original Medicare. Certain Medicare Advantage plans may also have varying monthly premiums. This could potentially make Medicare Advantage plans more affordable for some beneficiaries compared to traditional Medicare options, likely simplifying budgeting and possibly providing financial predictability.

Emergencies and Referrals

Medicare Advantage PPO plans let members visit any provider who accepts Medicare without referrals, even for specialist services. In contrast, Medicare Advantage HMO plans typically require referrals to see specialists, except in the case of emergencies. This structure likely ensures that members could receive coordinated care while maintaining flexibility for urgent needs.

All Medicare Advantage plans provide global emergency and urgent care coverage, ensuring members can receive care from any provider without prior authorization, regardless of network affiliation.

Summary

Navigating the available Medicare Advantage plans in South Carolina

Frequently Asked Questions

→ What types of Medicare Advantage plans are available in South Carolina?

In South Carolina, you will likely find various Medicare Advantage plans including HMO, PPO, and Special Needs Plans (SNPs) offered by providers like options cater to diverse healthcare needs, possibly ensuring that you can choose a plan that fits your lifestyle and medical requirements.

→ When can I enroll in a Medicare Advantage plan?

You can enroll in a Medicare Advantage plan during the Annual Enrollment Period from October 15 to December 7, your Initial Enrollment Period around your 65th birthday, or during Special Enrollment Periods due to specific life changes.

→ What additional benefits could Medicare Advantage plans offer?

Some Medicare Advantage plans may offer additional benefits such as dental, vision, and hearing services. These potential benefits may enhance your overall healthcare experience and promote a healthier lifestyle.

→ How could these costs compare between Medicare Advantage and Original Medicare?

Some Medicare Advantage plans may offer lower out-of-pocket costs and sometimes additional benefits compared to Original Medicare, which could provide broader access to providers but might lead to higher overall expenses. Therefore, the associated costs will likely depend on your healthcare needs and financial situation.

→ Do I need referrals to see specialists with Medicare Advantage plans?

Yes, whether you need referrals to see specialists with Medicare Advantage plans depends on your plan type; HMO plans usually require referrals, whereas PPO plans do not.

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 15 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.