Research Medicare Advantage Plans

Are you considering enrolling in a Medicare Advantage plan but feeling overwhelmed by the abundance of options and information available? This article could help you navigate the potential ins and outs of Medicare Advantage, making it easier for you to research Medicare Advantage plans and make an informed decision about your healthcare coverage.

From understanding the basics of Medicare Advantage plans to evaluating possible benefits, prior authorization requirements, and plan ratings, this article will provide you with the knowledge you may need to make the right choice for your healthcare needs.

Medicare Advantage, an alternative to Original Medicare, could offer a wide range of benefits and coverage options through private insurers. As the Medicare Advantage landscape continues to evolve, it’s essential to stay informed about the latest trends and developments in this area.

So, let’s unravel the complexities of the potential Medicare Advantage plans and help you make the best decision for your healthcare future by learning how to research Medicare Advantage plans effectively.

Key Takeaways

- Researching and comparing the potential Medicare Advantage plans could help beneficiaries make an informed decision about their healthcare coverage.

- Evaluating the potential provider networks, prescription drug coverage, supplemental benefits, and cost-sharing arrangements could be essential when selecting a plan that meets individual needs.

- Employers and those with chronic illnesses should consider care coordination and plan flexibility to ensure they may be able to receive the appropriate level of care.

Compare Plans in One Step!

Enter Zip Code

What are Medicare Advantage Plans

Some Medicare Advantage plans could act as an alternative to Original Medicare, which may provide additional benefits as part of the Medicare Advantage program. Offered by private insurers, these plans deliver all the benefits of Original Medicare (Parts A and B) and may also include supplemental benefits such as dental, vision, and hearing coverage.

As a result, some of the private Medicare Advantage plan options may have become increasingly popular among Medicare beneficiaries, with more opting for these Medicare Advantage plans to potentially enjoy some of the added benefits and the possibility of having reduced cost-sharing arrangements.

How Medicare Advantage Works

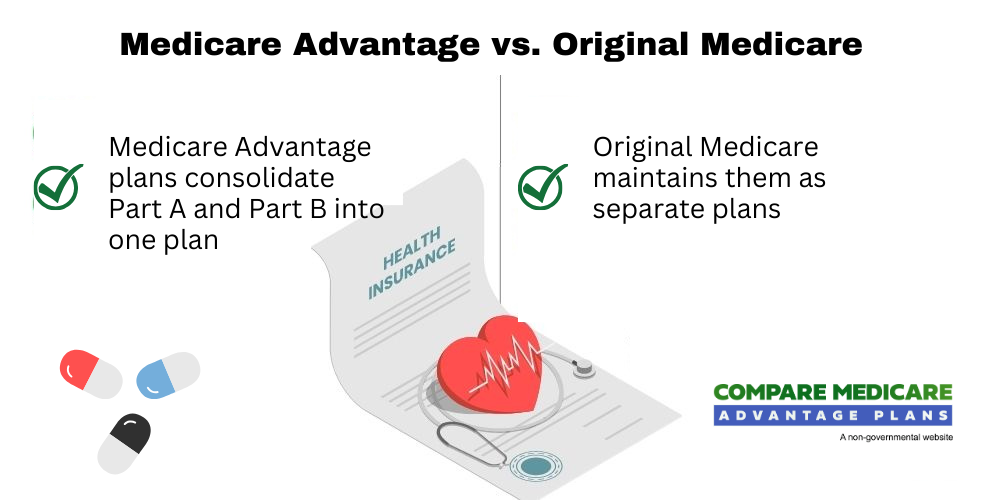

Medicare Advantage will likely combine Parts A and B by providing all the benefits of Original Medicare through a private plan that may be offered by an insurance company.

Some of these Medicare Advantage plans may also include Part D, which could furnish certain outpatient prescription drug coverage for individuals enrolled in these plans. In addition to the standard Medicare coverage, certain Medicare Advantage plans may also provide extra benefits, such as:

- Dental care

- Vision

These potential benefits could greatly enhance the overall healthcare experience for enrollees.

Bear in mind, that some of the costs that may be associated with certain Medicare Advantage plans may vary, including premiums, deductibles, copayments, and coinsurance. The exact costs will likely depend on the plan type and the individual insurance provider. Some Medicare Advantage plans may also have coverage that could differ based on the specific plan and insurance provider.

However, Medicare Advantage plans are required to provide the same services as Original Medicare, such as hospital stays, doctor visits, and prescription drugs.

Some plans may even offer additional benefits, like dental, vision, and hearing coverage. Hence, reviewing each plan’s details to comprehend its coverage is necessary.

Comparing Medicare Advantage to Original Medicare

Medicare Advantage could differ from Original Medicare in several ways. One possible distinction may lie in cost-sharing arrangements. While both programs may require beneficiaries to pay at least 20% of the Medicare-approved amount for Part B-covered services, some of the Medicare Advantage plans may provide reduced cost-sharing for certain services, which could make them more cost-effective for many enrollees.

Another notable difference might be in the provider networks. Certain Medicare Advantage plans could have a network of healthcare providers, while Original Medicare will likely allow beneficiaries to see any healthcare provider that accepts Medicare.

Moreover, some Medicare Advantage plans may also include additional benefits, such as vision, dental, and hearing coverage, which are not available under Original Medicare.

Private Insurers and Medicare Advantage

Private insurance companies could play a significant role in the Medicare Advantage landscape, as they contract with the government to offer certain plans.

Through an administrative and oversight process, the Centers for Medicare and Medicaid Services (CMS) will likely enter into contracts with private organizations to administer some of the benefits under Medicare Advantage. These companies may then be reimbursed by the federal government to provide Medicare-covered benefits to enrollees.

Private insurers might offer various coverage options in certain Medicare Advantage plans, including additional coverage for vision, hearing, and dental services.

However, there may be some trade-offs when obtaining a Medicare Advantage plan from a private insurer. Potential advantages to these plans could include the convenience of having certain benefits combined in one plan, potentially lower out-of-pocket costs compared to Original Medicare, and possibly having benefits that Original Medicare may not offer.

Evaluating Possible Benefits in Medicare Advantage Plans

Some of the Medicare Advantage plans may often include supplemental benefits, such as vision, dental, and hearing coverage. These benefits could greatly enhance the healthcare experience for enrollees, possibly making Medicare Advantage plans an attractive option for many.

Nonetheless, evaluating the potential benefits each plan could offer, as well as the associated cost-sharing arrangements, is key to making a knowledgeable choice about your healthcare coverage.

Types of Supplemental Benefits

Some common benefits that may be provided by Medicare Advantage plans could include:

- Eye care

- Hearing aids

In addition to these, general dental, vision, and hearing coverage may also be prevalent among certain Medicare Advantage plans, potentially offering enrollees comprehensive healthcare coverage that could go beyond what Original Medicare provides.

These additional benefits could make the Medicare Advantage plans seem more appealing to beneficiaries who may be seeking a well-rounded healthcare coverage option.

Possible Cost-Sharing for Supplemental Benefits

Cost-sharing for supplemental benefits in certain Medicare Advantage plans may vary depending on the specific plan and benefits offered. Reviewing the plan details and coverage documents may be necessary to understand the potential cost-sharing requirements for supplemental benefits.

This could help you determine if a particular plan could offer the right balance of cost and coverage to meet your healthcare needs.

In-Home Support Services and Special Needs Plans (SNPs)

Special Needs Plans (SNPs) will likely be designed to provide additional support for beneficiaries who may have specific needs.

These plans could offer tailored care and support for individuals with particular needs, which could greatly enhance the healthcare experience for enrollees.

Taking into account the availability of SNPs and their associated benefits, chronically ill enrollees can make a knowledgeable choice about their healthcare coverage.

Navigating Prior Authorization Requirements

Prior authorization may be a common requirement in certain Medicare Advantage plans, which could affect access to certain services. This medical management technique will likely require providers to obtain approval from the health plan before certain healthcare services may be provided, ensuring that the services are medically necessary.

Understanding your Medicare Advantage plan’s specific prior authorization requirements could help you navigate the healthcare system and guarantee you receive the care you need.

Common Services Requiring Prior Authorization

Services that could require prior authorization in Medicare Advantage plans may include Part B drugs, skilled nursing facility stays, and inpatient hospital stays.

The process for obtaining prior authorization will likely involve submitting a request for approval, along with all relevant medical documentation, which is then evaluated by the health plan to determine if the requested service is medically necessary.

Knowing the services that may require prior authorization in your plan could help ensure you receive the necessary care without unanticipated out-of-pocket expenses.

Preventive Services and Prior Authorization

Preventive services may be less likely to require prior authorization in certain Medicare Advantage plans, as these services could be designed to prevent the delivery of inappropriate or low-value care.

Comprehending the potential prior authorization requirements for preventive services in your Medicare Advantage plan may guarantee your receipt of necessary care to maintain your health and well-being.

Tips for Managing Prior Authorization Requirements

To manage prior authorization requirements, it’s important to stay informed about your plan’s policies and communicate with your healthcare providers.

Providers must work with the health plan to submit a request for approval, and the plan will likely evaluate the request to determine if it meets the required criteria. If approval is granted, the service may be provided. However, if not approved, the provider may have to explore other alternatives or challenge the decision.

Knowing the prior authorization process and collaborating closely with your healthcare providers could help ensure you receive the care you need without unnecessary delays or high out-of-pocket expenses.

Analyzing Medicare Advantage Plan Ratings

Medicare Advantage plans are rated on a 1 to 5-star scale, with higher ratings indicating better quality and performance. These ratings may consider certain factors such as customer service, clinical outcomes, and member satisfaction, which could help beneficiaries make informed decisions about their healthcare coverage.

Comprehending the star rating system and considering plan ratings in your decision-making process could help to ensure you choose a high-quality plan that meets your healthcare needs.

Understanding the Star Rating System

The star rating system evaluates Medicare Advantage plans will likely be based on factors like customer service, clinical outcomes, and member satisfaction. Plans with four or more stars may be eligible to receive annual bonus payments through the Quality Bonus Program, which will likely provide an incentive for plans to improve their quality performance and could offer beneficiaries an easy way to evaluate the overall quality of these plans.

Getting acquainted with the star rating system could help you make knowledgeable decisions about your healthcare coverage and choose a plan that best meets your needs.

Factors Affecting Plan Ratings

Plan ratings may be affected by:

- Possible changes in performance measures

- Changes to payment methodologies

- Calculation of rates based on fee-for-service actuarial equivalent cost-sharing factors

- Benchmarks

- Risk adjustment

- Prescription drug plan base

Taking these potential factors into account could help you make knowledgeable decisions about your healthcare coverage and choose a plan that best meets your needs.

Choosing a High-Quality Plan

When choosing a Medicare Advantage plan, members may want to consider the following factors:

- Star rating

- Costs

- Coverage

- Provider networks

- Supplemental benefits

- Prescription drug coverage

By comparing the possible plan options and taking these factors into account, you can make an informed decision about your healthcare coverage and choose a plan that best meets your needs.

Possible Cost Considerations for Medicare Advantage Enrollees

The potential costs for Medicare Advantage enrollees may vary, with possible factors like premiums, rebates, and out-of-pocket limits that could affect overall expenses. Understanding some of these potential cost considerations and comparing different plan options could help you make a knowledgeable choice about your healthcare coverage, selecting a plan that best suits your needs and budget.

Premiums and Rebates

Many Medicare Advantage enrollees may enjoy some of the following benefits:

- Plans may offer rebates to offset costs.

- Plans may provide enrollees with additional benefits.

Taking into account the potential plan rebates could help you make a knowledgeable choice about your healthcare coverage and select a plan that best suits your needs and budget.

Possible Out-of-Pocket Limits and Cost Sharing

Out-of-pocket limits and cost-sharing arrangements could impact overall healthcare spending for Medicare Advantage enrollees.

Understanding these potential factors could help you make an informed decision about your healthcare coverage and choose a plan that best meets your needs and budget.

Balancing Costs with Coverage Needs

To balance costs with coverage needs, you may need to compare plan options and consider factors like possible benefits and provider networks.

Carefully evaluating these factors could help you make a knowledgeable choice about your healthcare coverage and select a plan that best suits your needs and budget.

Enrollment Trends and Implications

Medicare Advantage enrollment will likely continue to grow, with more beneficiaries choosing these plans over Original Medicare. This enrollment growth could lead to advancements for the Medicare program, such as decreased program costs and rate-setting issues.

Growth in Medicare Advantage Enrollment

Enrollment in Medicare Advantage plans will likely increase as more beneficiaries choose these plans over Original Medicare. Some factors that may contribute to this growth may include:

- Increased preference for managed care

- Attraction of extra benefits that might be offered by certain plans

- Diversification of enrollment among Black, Hispanic, and low-income individuals.

Possible Financial Implications of Enrollment Trends

This enrollment growth could lead to financial advantages for the Medicare program. To address some of these benefits, the Medicare Payment Advisory Commission, along with researchers, suggest strategies for improving rate setting to ensure the sustainability of Medicare Advantage plans, taking into account the enrollment data.

Strategies for Improving Medicare Advantage Rate Setting

Researchers suggest a range of strategies for improving rate setting in Medicare Advantage plans, such as:

- Addressing upcoding

- Optimizing the payment process

- Improving population health management

- Enhancing the consumer experience

- Increasing transparency

Implementing these strategies might assist policymakers and healthcare providers in ensuring the long-term sustainability of Medicare Advantage plans.

Researching and Comparing Medicare Advantage Plans

Researching and comparing Medicare Advantage plans may help beneficiaries make informed decisions about their healthcare coverage.

Utilizing publicly available data, assessing provider networks and potential prescription drug coverage, and considering the needs of chronically ill enrollees and employer-sponsored plans could help you select the plan that best suits your healthcare needs and budget.

Utilizing Publicly Available Data

Members may use publicly available data, such as CMS resources, to compare potential plan options and costs. Accessing this information can help you make knowledgeable decisions about your healthcare coverage and select a plan that best suits your needs.

Evaluating Provider Networks and Prescription Drug Coverage

Evaluate potential factors like provider networks and prescription drug coverage when choosing a plan. Considering these factors could help ensure you receive the care you need from the providers you trust, and that your prescription medications may be covered by your plan.

Considerations for Chronically Ill Enrollees and Employer Plans

For chronically ill enrollees and those with employer-sponsored plans, they may want to consider additional factors like care coordination and plan flexibility. Taking these potential factors into account could help ensure they receive the appropriate level of care and support for their specific healthcare needs.

Summary

Understanding the potential complexities of Medicare Advantage plans is crucial for making informed decisions about your healthcare coverage.

By considering possible factors such as plan ratings, costs, coverage, and provider networks, you could choose a plan that best meets your needs and budget. Stay informed, research your options, and make the right choice for your healthcare future.

Frequently Asked Questions

→ Why are people choosing Medicare Advantage plans?

People may choose Medicare Advantage plans due to the lack of prior authorization and quick payments from insurers.

→ What is the biggest advantage of Medicare Advantage?

The biggest advantage of Medicare Advantage might be the broad range of choices for doctors and medical offices, as well as possible reduced costs for coverage and complex plan offerings.

→ What are 4 types of Medicare Advantage plans?

Medicare Advantage Plans come in four varieties: Health Maintenance Organization (HMO) plans, Preferred Provider Organization (PPO) plans, Private Fee-for-Service (PFFS) plans, and Special Needs plans (SNPs).

→ Why are they pushing Medicare Advantage plans?

Medicare Advantage plans might have become increasingly popular due to their lower cost compared to Medicare supplements. Enrollment in these plans has more than doubled since 2013, potentially offering further incentives for people to consider them.

→ What are the main differences between Medicare Advantage and Original Medicare?

Some of the Medicare Advantage plans may feature different cost-sharing arrangements, less restrictive provider networks, and additional benefits such as vision, dental, and hearing coverage which may not be offered with Original Medicare.

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 15 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.