What’s Best: Medicare vs. Medicare Advantage Plans – Understanding the Basics

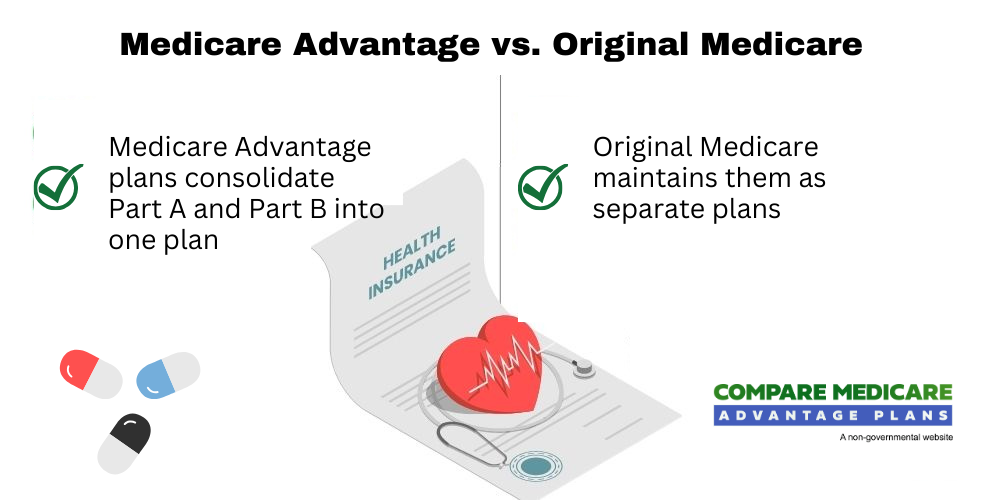

Grasping the basics is crucial for making informed decisions. Original Medicare consists of multiple separate components known as Parts A and B. Part A covers inpatient hospital care, skilled nursing facility care, hospice, and some home health care. Part B covers outpatient care, preventive services, ambulance services, and some medical equipment. This foundational coverage is straightforward but may leave gaps in areas like prescription drugs and routine dental services.

On the other hand, Medicare Advantage Plans, also known as Part C, are offered by private insurance companies approved by Medicare. These plans bundle together the services provided by Parts A and B and often include additional benefits such as:

- Dental care

- Vision care

- Hearing care

Many also incorporate Medicare prescription drug coverage, providing a one-stop-shop for comprehensive healthcare needs and various plan choices.

In 2025, the average beneficiary had 42 Medicare Advantage plans to choose from, with 51% of eligible beneficiaries enrolled in such plans. This popularity is no accident; many find the allure of additional benefits and lower out-of-pocket costs appealing. However, it’s crucial to note that Medicare Advantage plans restrict purchasing a Medigap plan and typically have provider network limitations compared to Original Medicare.

While both Medicare options cover essential medical services such as blood work, diagnostic tests, doctor visits, hospitalizations, outpatient surgery, and medical care, the choice between them often hinges on personal healthcare needs and financial situations. Whether you value the flexibility of Original Medicare or the bundled benefits of Medicare Advantage, understanding these basics sets the stage for deeper exploration.

Cost Structures: Comparing Monthly Premiums and Out-of-Pocket Costs

When comparing Medicare options, cost structures are a critical consideration. Medicare Part B premiums are projected to increase by 11.6% in 2026, while Part D premiums are expected to rise by about 6%. These increases can significantly impact your monthly budget, making it essential to understand the full scope of potential expenses, including the part b premium.

Interestingly, the average monthly premiums for Medicare Advantage are expected to drop from $16.40 in 2025 to $14 in 2026. This reduction highlights one of the primary financial advantages of Medicare Advantage plans, which are often subsidized, leading to lower medicare premiums compared to traditional Medicare plans. However, it’s not just about the premiums; out-of-pocket costs play a significant role as well.

Unlike Original Medicare, which does not have a maximum fair price on out-of-pocket costs, Medicare Advantage plans usually have an annual limit on out-of-pocket expenses for covered services. This cap can provide peace of mind, knowing that your financial exposure is limited.

The projected out-of-pocket maximum for Medicare Part D will rise to $2,100 in 2026. Additionally, some Medicare Advantage plans may offer extra cost savings on prescription costs compared to Medicare Part D, depending on the plan’s structure.

Coverage Differences: What Services Are Included?

When it comes to coverage, the differences between Original Medicare and Medicare Advantage are stark. Original Medicare primarily covers essential medical services but falls short in areas such as:

- Routine dental care

- Hearing aids

- Vision correction

- Emergency medical services received abroad are generally not covered by Original Medicare, which can be a significant limitation for frequent travelers.

Medicare Advantage plans, however, often provide additional benefits that are not part of Original Medicare. These can include services for:

- Dental

- Vision

- Hearing

- Most Medicare Advantage plans incorporate prescription drug coverage, making them a more comprehensive option for those who need regular medications.

The formulary, or list of covered drugs, can vary significantly between Medicare Advantage plans and standalone Medicare Part D plans.

Flexibility in Provider Access and Network Restrictions

Flexibility in provider access is another critical factor in choosing between Original Medicare and Medicare Advantage. Original Medicare allows beneficiaries to visit any doctor or hospital that accepts Medicare, providing nationwide access. This unrestricted access means that you can see any specialist or primary care doctor without worrying about network limitations.

In contrast, Medicare Advantage Plans typically require members to use a plan’s network of providers, which may limit access to specialists without a referral. The limited provider networks can change, affecting continuity of care. While emergency care under Medicare Advantage is typically covered even when receiving treatment from out-of-network providers, the need for prior referrals and network restrictions can be cumbersome.

Prescription Drug Coverage: Medicare Part D vs. Medicare Advantage

Prescription drug coverage is a crucial component of healthcare for many seniors. Beneficiaries can choose to enroll in a separate Medicare Part D plan in addition to Original Medicare, but this option is not available if they are enrolled in most Medicare Advantage plans. This means that those on Medicare Advantage often have their cover prescription drugs bundled into their overall health plan, simplifying their coverage.

Medicare Part D provides drug coverage through standalone plans offered by private insurers, allowing Original Medicare beneficiaries to add this vital coverage. However, the cost structure for drug coverage can differ significantly between Part D drug plans and Medicare Advantage. Medicare Advantage plans often include drug coverage as part of the overall health plan, potentially leading to cost savings on prescriptions depending on the plan’s structure.

Both Medicare options have their pros and cons when it comes to prescription drugs. While Medicare Advantage offers the convenience of bundled coverage, it may also come with formulary restrictions and network limitations. Original Medicare with Part D, on the other hand, provides flexibility but can lead to higher out-of-pocket costs without the protections of an all-inclusive plan.

Geographic Considerations: Nationwide Access vs. Local Networks

Geographic location plays a significant role in the accessibility and convenience of Medicare plans. Original Medicare offers the freedom to receive care from any provider that accepts Medicare, anywhere in the U.S. This nationwide access is particularly beneficial for those who travel frequently or live in multiple locations throughout the year.

Medicare Advantage plans, however, are often restricted to particular regions, which can limit access to services for beneficiaries living in rural areas. While emergency care is covered by Medicare Advantage plans regardless of travel location within the United States, routine care may be limited to the plan’s network. This can pose challenges for those who require consistent access to specific healthcare providers across different regions.

Prior Authorizations and Administrative Burden

The administrative aspects of Medicare plans can significantly impact your healthcare experience. Medicare Advantage plans have the authority to impose stricter prior authorization requirements compared to Original Medicare. These requirements can lead to delays in treatment, impacting patient care and increasing the administrative burden on both patients and providers.

The CMS Interoperability and Prior Authorization Final Rule aims to enhance the efficiency of prior authorization processes, which is a significant aspect of Medicare Advantage plans. The new rule emphasizes improving data sharing to reduce the burden associated with prior authorizations for all parties involved. Despite these efforts, the administrative processes for prior authorization in Medicare Advantage can still be cumbersome.

The Centers for Medicare & Medicaid Services (CMS) is actively working to reduce these administrative burdens. However, the need for prior authorizations in Medicare Advantage can still lead to unexpected delays and potential gaps in care. Understanding these administrative requirements is crucial for making an informed decision about your healthcare coverage.