What Is Medicare Part C (Medicare Advantage)?

Medicare Advantage Plans, also known as Part C, are health plans offered by private companies approved by Medicare. These plans provide all the benefits of Medicare Part A (hospital insurance) and Part B (medical insurance), often including Medicare Part D (prescription drug coverage) as well. This comprehensive coverage is a significant draw for many beneficiaries, as it simplifies the management of healthcare services by consolidating them into one plan.

There are various types of Medicare Advantage Plans available, including:

- Health Maintenance Organizations (HMOs)

- Preferred Provider Organizations (PPOs)

- Regional PPOs

- Private Fee-for-Service (PFFS) plans

Each type comes with its own set of rules and network restrictions, which must adhere to the regulations established by Medicare. Choosing the right plan requires knowledge of these options and how they align with your healthcare needs.

How Medicare Advantage Can Combine Parts A, B, and D

Medicare Advantage plans, also known as Part C, typically integrate coverage for hospital services (Part A), medical services (Part B), and prescription drugs (Part D) into one seamless plan. This bundling not only simplifies the healthcare process for beneficiaries but also often includes additional benefits that go beyond what Original Medicare offers, such as dental and vision care.

Many Medicare Advantage plans require beneficiaries to use a network of providers, which has the following implications:

- Potentially limits access to certain services compared to Original Medicare.

- Streamlines services and reduces costs.

- May limit your choices of doctors and hospitals.

Why Many Beneficiaries Are Choosing Part C in 2026

The landscape of healthcare is continually evolving, and in 2026, many beneficiaries are gravitating towards Medicare Advantage Plans for several compelling reasons. Rising medical costs and the introduction of new technologies are major motivators, as these plans often offer more predictable costs and integrated services. Additionally, the open enrollment period has generated increased interest as beneficiaries seek to manage their healthcare expenses more effectively.

Advocacy by prominent figures in the new administration and the provisions of the Inflation Reduction Act, aimed at lowering drug prices, have also made Medicare Advantage more attractive. These factors, combined with the extra benefits that most Medicare Advantage plans offer beyond traditional Medicare, have led to a surge in popularity for Part C in 2026.

Key Changes to Medicare Advantage Plans in 2026

As we look ahead to 2026, several key changes to Medicare Advantage Plans are coming into effect. These changes encompass adjustments in premiums, out-of-pocket costs, benefits, and coverage options.

Being aware of these updates helps in making informed decisions about your healthcare health policy plan.

Average Premiums and Out-of-Pocket Costs

In 2026, the average monthly premiums for Medicare Advantage plans are expected to decrease by approximately 14%, dropping from $16.40 to $14.00. This reduction in Medicare premiums is a welcome change for many beneficiaries, potentially making these plans more affordable. However, it’s important to consider that the Part B premium is projected to rise from $185 to $206.50, which could offset some of the savings from lower Medicare Advantage premiums.

Additionally, the catastrophic threshold for Medicare Part D, which functions like an out-of-pocket maximum, will increase from $2,000 to $2,100 in 2026. This means that while premiums may be lower, beneficiaries could still face higher overall costs due to increased out-of-pocket limits and rising Part B premiums.

Updates From the Inflation Reduction Act

The Inflation Reduction Act brings significant updates to Medicare Advantage plans in 2026, particularly in the realm of prescription drug costs. One major change is the waiver of Medicare Part D deductibles for certain adult vaccines and covered insulin products. This means that beneficiaries will no longer need to pay deductibles for these essential medications, making them more accessible and affordable.

Additionally, the Medicare Drug Price Negotiation Program will establish maximum fair prices for selected medications, further reducing drug costs for beneficiaries. Medicare Advantage plans will also be required to offer payment options for prescription drugs, allowing beneficiaries to spread out costs over the year.

These updates are designed to make prescription medications more affordable and manageable for beneficiaries.

New Benefits and Coverage Options for 2026

Medicare Advantage plans in 2026 will feature several new benefits and enhanced coverage options. For instance, Blue Cross Medicare Advantage plans will include additional services like wellness programs, hearing aids, and vision care. These enhancements provide a more comprehensive coverage experience, addressing a broader range of healthcare needs.

Moreover, the Medicare Plan Finder tool will be improved with new features, including an AI-powered prescription cost estimator to help beneficiaries understand medication costs across local pharmacies. These advancements make it easier for beneficiaries to compare plans and providers, ensuring they choose the best coverage for their specific healthcare needs.

Availability of Plans by State and County

The availability of Medicare Advantage plans can vary significantly by state and county, reflecting the local healthcare market and regulations. Blue Cross and Blue Shield, for instance, offers various Medicare Advantage options that can be tailored to individual needs based on the availability in specific regions. To determine the specific plans available, individuals can enter their ZIP Code on the Blue Cross and Blue Shield website.

Each Blue Cross Blue Shield company operates independently, meaning the details of Medicare Advantage plans, including premiums and benefits, may differ from one region to another. This regional variation allows beneficiaries to find plans that best meet their healthcare needs within their local market.

Prescription Drug Coverage in Medicare Advantage

Many Medicare Advantage plans include prescription drug coverage under Part D, which can significantly affect overall healthcare prescription costs and medicare costs. With a cap on out-of-pocket expenses for covered drugs set at $2,000 starting in 2025, beneficiaries can better manage their medication costs.

Including prescription drug coverage in a plan provides comprehensive care and financial predictability throughout the year.

What Do Medicare Advantage Plans Cover?

Medicare Advantage plans offer a wide range of coverage that often extends beyond what Original Medicare provides. These additional benefits can be a deciding factor for many beneficiaries. Most Medicare Advantage plans include extra services such as:

- Dental benefits

- Vision benefits

- Hearing benefits

- Wellness programs that promote preventive care and healthy living.

Understanding this comprehensive coverage is essential for making an informed decision.

Hospital and Medical Services

Blue Cross Blue Shield Medicare Advantage plans include:

- All services covered under Parts A and B of Original Medicare

- Additional benefits like wellness programs

- Typically lower overall cost sharing

- An annual cap on out-of-pocket expenses, providing better cost predictability compared to Original Medicare

This means beneficiaries can enjoy comprehensive medical care without the financial uncertainty often associated with healthcare costs.

Medicare Advantage plans from Blue Cross may include:

- A network of healthcare providers, requiring members to check if their doctors participate in the plan.

- Prescription drug coverage, which can lead to varying costs based on specific plan details.

- Network-based care that ensures coordinated services and often results in lower overall medical costs for beneficiaries.

Prescription Drug Coverage in 2026

In 2026, the average premium for Medicare Advantage plans that include prescription drug coverage is estimated to drop from $13.32 in 2025 to $11.50. This decrease, coupled with the actions by CMS to control costs for Medicare prescription drug coverage, ensures that nearly all Medicare beneficiaries will have access to affordable prescription drug plan options.

The availability of such plans simplifies the healthcare experience for beneficiaries, providing comprehensive coverage at a lower cost.

Extra Benefits (Dental, Vision, Hearing, Fitness, OTC)

Many Medicare Advantage plans offer a variety of extra benefits that are not typically covered by Original Medicare, including medicare covered services such as medicare supplement plans:

- Dental

- Vision

- Hearing

- Fitness programs

- Over-the-counter (OTC) allowances

These extra benefits can significantly enhance the overall healthcare experience and provide added value to beneficiaries.

Medicare Advantage Costs in 2026

Monthly premiums for Medicare Advantage plans vary significantly by region and provider, reflecting local healthcare market conditions. However, the average monthly premium for Medicare Advantage plans is projected to decrease from $16.40 in 2025 to $14.00 in 2026. This reduction makes these plans more affordable for beneficiaries, allowing them to access comprehensive healthcare services at a lower cost.

Deductibles and Copayments

Many beneficiaries experience higher out-of-pocket expenses due to increased copayments and deductibles associated with certain Medicare Advantage plans. However, many plans are expected to keep their copayment structures similar to previous years, providing predictability in out-of-pocket costs for beneficiaries. This means that while some costs may increase, the overall structure of deductibles and copayments will remain consistent, allowing beneficiaries to plan their healthcare expenses more effectively.

Certain Medicare Advantage plans may impose d deductible, which are the amounts members must pay out-of-pocket before coverage begins. Copayments are often required for specific services, such as visits to a doctor’s office.

Despite these annual costs, Medicare Advantage plans typically include an annual cap on out-of-pocket expenses, providing financial predictability and protection against high medical costs.

Out-of-Pocket Maximums

Medicare Advantage plans are required to set a cap on out-of-pocket costs, which can provide significant financial protection against high medical expenses. In 2026, these plans must adhere to specific out-of-pocket maximum limits, ensuring that beneficiaries do not pay more than a predetermined amount for covered services.

For 2026, the maximum out-of-pocket limit for Medicare Advantage plans will be capped at $8,300 for in-network services and up to $11,800 for combined in- and out-of-network services. This cap offers peace of mind and financial security for beneficiaries.

Medicare Advantage Eligibility and Enrollment in 2026

To enroll in a Medicare Advantage plan, individuals must possess both Medicare Part A and Part B, reside within the plan’s service area, and be a U.S. citizen or a legal resident. Understanding these eligibility criteria is crucial for those considering Medicare Advantage, as it ensures they meet the necessary requirements for enrollment.

Who Qualifies for Part C

Individuals eligible for Medicare Advantage must meet specific criteria, including:

- Age

- Disability status

- Being enrolled in both Medicare Part A and Part B

- Residing in the plan’s service area

- Being U.S. citizens or legal residents.

Knowing these qualifications ensures potential beneficiaries are aware of their eligibility for Medicare Advantage plans.

When to Enroll (Initial, Special, and Annual Enrollment Periods)

There are multiple enrollment periods for Medicare Advantage, including the Initial Enrollment Period, Annual Coordinated Election Period, and various Special Election Periods. The Initial Enrollment Period lasts for seven months, beginning three months before the individual turns 65 and continuing for three months after. This period is crucial for new beneficiaries to enroll in Medicare Advantage without penalties.

The Annual Enrollment Period, running from October 15 to December 7 each year, allows beneficiaries to switch or enroll in Medicare Advantage plans. Special Enrollment Periods apply under specific circumstances, such as moving or losing other coverage, providing flexibility for beneficiaries to adjust their plans as needed.

Awareness of these periods allows beneficiaries to make timely decisions about their healthcare coverage.

How to Switch or Drop a Plan

Beneficiaries can change or discontinue their Medicare Advantage plan during designated enrollment windows, ensuring they meet the specific criteria for switching. Key points include:

- The Medicare Advantage Open Enrollment Period runs from January 1 to March 31.

- This period allows those already enrolled in a plan to switch plans.

- Beneficiaries can also return to Original Medicare during this time.

Special Enrollment Periods also provide opportunities to change plans under certain conditions, such as moving or losing coverage. Knowing these options helps beneficiaries make informed decisions about their healthcare plans.

Comparing Medicare Part C Plans in 2026

Comparing Medicare Part C plans can be overwhelming due to the variety of options available. In 2026, Medicare Advantage plans and medicare plans offer various choices that cater to different healthcare needs, allowing beneficiaries to choose plans that align with their preferences and coverage requirements.

Considering key factors for comparison is vital for selecting the best compare plan options.

HMO vs PPO vs PFFS vs SNP Plans

Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee-for-Service (PFFS) plans, and Special Needs Plans (SNPs) differ as follows:

- HMOs typically require members to select a primary care doctor and get referrals to see specialists.

- PPOs offer greater flexibility in choosing healthcare providers without needing referrals.

- PFFS plans allow beneficiaries to visit any Medicare-approved provider, although they may have specific payment terms that need to be followed.

- SNPs are designed for individuals with specific health conditions and must offer Medicare drug coverage.

Recognizing these differences is essential for choosing the right plan. For instance, while HMOs might offer lower costs, they come with network restrictions that could limit access to certain providers.

On the other hand, PPOs provide more flexibility but may come with higher costs for out-of-network services. Each type has its own advantages and potential drawbacks, making it important to consider personal healthcare needs and preferences when choosing a plan.

Regional vs National Plan Options

Regional Medicare Advantage plans generally cater to specific geographical areas, offering benefits tailored to local healthcare needs. These plans often provide services that reflect the unique requirements of the region, which can be beneficial for residents. However, regional plans may have limited provider networks, which could restrict access to certain doctors and facilities.

National Medicare Advantage plans, on the other hand, offer coverage across multiple states, providing broader access to healthcare services. These plans typically have more diverse provider networks, which can lead to greater flexibility in choosing healthcare providers.

The choice between regional and national plans can significantly impact the availability of healthcare providers and facilities, making it essential to consider these factors when comparing plan options, plan choices, and the plan’s network.

How to Use the Medicare Plan Finder in 2026

The Medicare Plan Finder tool is designed to help beneficiaries compare various Medicare Advantage plans based on their personal healthcare needs and preferences. For 2026, the tool has been updated with new features, including an AI-powered prescription cost estimator to help users determine medication costs at local pharmacies. These advancements make it easier for beneficiaries to find and compare plans that meet their specific needs.

Additionally, the Medicare Plan Finder allows beneficiaries to compare plans based on costs, coverage, and provider networks, streamlining the decision-making process. The tool will be updated with the latest 2026 health and prescription drug plan information by October 1, 2025, ensuring that beneficiaries have access to the most current data when making their decisions.

Utilizing this tool during the Open Enrollment period can help beneficiaries find the best plan for their healthcare needs.

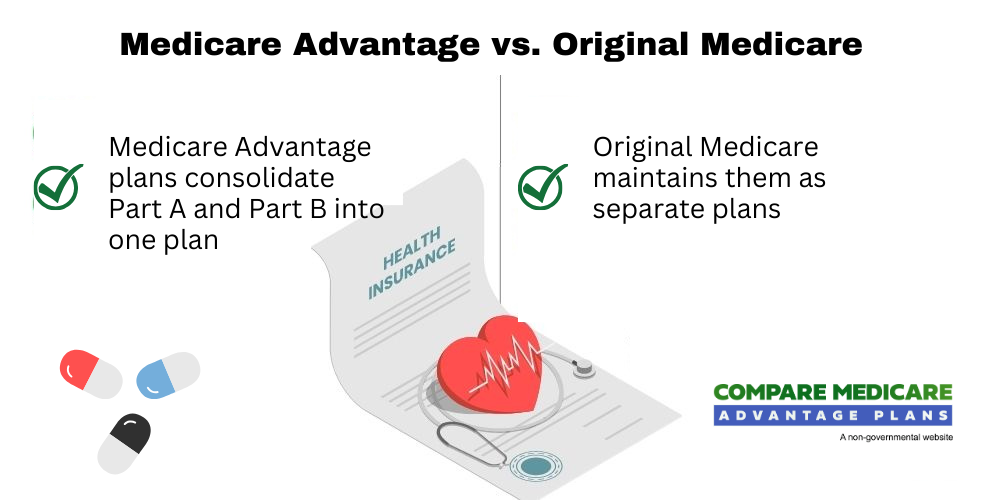

Medicare Advantage vs Original Medicare in 2026

In 2026, Medicare beneficiaries will have the option to choose between Original Medicare and Medicare Advantage, each offering different cost structures and medicare coverage options, as well as various medicare policy choices.

Knowing the differences between these two options is crucial for making an informed decision about healthcare coverage.

Cost Differences

Medicare Advantage plans often feature:

- Set copay amounts for services, in contrast to Original Medicare’s percentage-based costs, allowing beneficiaries to anticipate more predictable healthcare expenses.

- Typically lower monthly premiums compared to Original Medicare.

- Additional out-of-pocket costs for services.

- An out-of-pocket maximum limit that provides an added layer of financial protection, which is not available with Original Medicare.

While Original Medicare covers hospital and medical services, Medicare Advantage policies can vary widely in how costs are structured and the benefits offered. Cost-sharing in Medicare Advantage plans can include copayments or coinsurance, meaning beneficiaries may pay different amounts based on the type of service received. Recognizing these cost differences helps beneficiaries choose the plan that best fits their financial situation.

Coverage and Flexibility

Medicare Advantage plans typically offer additional benefits beyond what Original Medicare provides, including dental, vision, and wellness programs. However, these plans often have provider networks that limit beneficiaries to certain doctors and facilities, whereas Original Medicare allows access to any healthcare provider nationwide that accepts Medicare. This difference in provider access can significantly impact the flexibility of healthcare choices.

While Medicare Advantage plans may offer more comprehensive coverage, including extra benefits that Original Medicare does not cover, they also come with network restrictions that could limit access to care if traveling or living in different areas. Balancing additional benefits with provider flexibility is key when deciding between Medicare Advantage and Original Medicare.

Which Option Is Right for You?

Choosing between Medicare Advantage and Original Medicare should consider both healthcare needs and financial circumstances. For individuals who prioritize additional benefits like dental and vision care, Medicare Advantage may be the better choice. However, those who prefer the flexibility to visit any doctor who accepts Medicare might find Original Medicare more suitable.

Travelers might prefer Original Medicare due to its nationwide coverage, while Medicare Advantage plans may have geographical restrictions. Evaluating personal healthcare needs, budget, and preferences is essential for making an informed decision between these two options.

Pros and Cons of Medicare Part C in 2026

Medicare Part C, or Medicare Advantage, offers several pros and cons that beneficiaries should consider. These plans provide additional benefits and financial predictability but also come with potential limitations.

Recognizing these advantages and drawbacks is essential for making an informed decision.

Advantages of Medicare Advantage Plans

Medicare Advantage plans often include additional services beyond traditional Medicare, such as dental, vision, and hearing coverage. These plans also typically offer a cap on out-of-pocket expenses, providing financial security for beneficiaries. In 2026, the average premium for Medicare Advantage plans is expected to decrease, making these plans more affordable for beneficiaries.

Additionally, many Medicare Advantage plans include:

- Prescription drug coverage, simplifying the coverage experience for beneficiaries

- Wellness programs

- Fitness memberships

- Transportation services

These features enhance the overall health care experience.

These benefits make Medicare Advantage an attractive option for many beneficiaries.

Potential Drawbacks to Consider

One potential drawback of Medicare Advantage plans is the reduction in supplemental benefits, which could limit the options available to enrollees. Additionally, some plans may have limited provider networks, restricting access to doctors and specialists. This can be a significant concern for beneficiaries who prefer broader provider access. The drawbacks include:

- Reduction in supplemental benefits, limiting options for enrollees

- Limited provider networks, restricting access to doctors and specialists

- Concerns for beneficiaries who prefer broader provider access

Beneficiaries may also face higher out-of-pocket costs for certain services under Medicare Advantage compared to Original Medicare. Medicare Advantage plans often require prior authorization for specific services, which can delay access to care.

Being aware of these potential limitations is crucial for making an informed decision about Medicare Advantage plans.